Welcome to a world where understanding insurance becomes simpler, smarter, and incredibly empowering! Imagine cutting through the confusion of policies and rates in North Carolina with insightful clarity. Our guide is crafted to enlighten and elevate your insurance knowledge, transforming you from a passive premium payer into a savvy, informed decision-maker.

By unraveling the intricacies of insurance types, diving deep into the factors affecting costs, and comparing top providers, you’ll embark on a journey that not only saves you money but also ensures you make the most informed choices for your personal needs. Let’s unlock the incredible potential of insurance in North Carolina together!

Understanding Insurance Basics

When exploring the realm of insurance in North Carolina, it’s crucial to have a solid grasp of the basics. Understanding different types of coverage and the factors affecting your rates can empower you to make informed decisions.

In North Carolina, insurance isn’t just a necessity—it’s a strategic tool that can protect your assets, health, and future. Let’s dive deep into the core components that shape your insurance landscape.

Different Types of Insurance Available in NC

North Carolina offers a variety of insurance types tailored to meet diverse needs. From safeguarding your vehicle on the open roads to ensuring the health and well-being of your family, there are multiple options to consider:

- Auto Insurance: Covers damages and liabilities relating to vehicles.

- Health Insurance: Ensures access to medical services when needed.

- Homeowners Insurance: Protects against property damage and theft.

- Life Insurance: Provides financial support to beneficiaries.

- Renters Insurance: Offers coverage for personal belongings in a rented property.

Each type of insurance serves a different purpose, ensuring a comprehensive shield against a range of uncertainties.

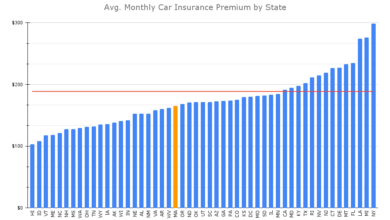

Factors Influencing Insurance Rates in NC

The cost of insurance in North Carolina can be influenced by a variety of factors. Being aware of these elements can help you secure the best possible rates:

“Your personal details, choice of coverage, and external influences all play a part in determining your insurance premiums.”

- Personal Factors: Age, driving history, and credit score can affect rates.

- Coverage Choices: Opting for high coverage can increase costs.

- Location: Urban areas may face higher premiums due to increased risk.

- Economic Conditions: Inflation and market trends can impact rates.

Standard Coverage Options in Insurance Policies

Understanding standard coverage options is crucial to tailoring an insurance policy that suits your needs. Below is a comparison of common coverage types, their descriptions, and their importance:

| Coverage Type | Description | Importance |

|---|---|---|

| Liability Coverage | Protects against claims for damages you’re legally responsible for. | Essential for financial protection against lawsuits and claims. |

| Collision Coverage | Covers damage to your vehicle from at-fault accidents. | Important for repairing or replacing your car post-accident. |

| Comprehensive Coverage | Provides coverage against theft or non-collision damages. | Vital for safeguarding against unexpected non-accident events. |

| Medical Payments | Covers medical expenses for policyholders. | Crucial for ensuring medical bills are handled efficiently. |

Comparing Insurance Providers

Choosing the right insurance provider in North Carolina can feel like an overwhelming decision, but it all boils down to understanding your options. Let’s demystify this process by exploring a side-by-side comparison of the top players in the market.

By evaluating customer ratings, coverage options, and special discounts, you can make an informed decision that aligns with your needs and budget.

Top Insurance Providers in NC: A Closer Look

| Provider Name | Customer Rating | Coverage Options |

|---|---|---|

| Blue Cross Blue Shield NC | 4.5/5 | Health, Dental, Vision, Life |

| Allstate | 4.3/5 | Auto, Home, Renters, Motorcycle |

| Nationwide | 4.2/5 | Auto, Home, Pet, Business |

| State Farm | 4.6/5 | Auto, Home, Health, Life |

Criteria for Evaluating Insurance Providers

Understanding the criteria for evaluation is key to making the best choice. Generally, customers look at:

- Financial Strength: A company’s ability to pay out claims even in economically challenging times.

- Coverage Options: The range of coverage types that suit different needs and lifestyles.

- Pricing: How competitive the rates are compared to the market.

- Customer Service Quality: The accessibility and responsiveness of customer support.

These factors combined can heavily influence your peace of mind and financial security.

Exclusive Discounts and Benefits

Many insurance providers offer enticing discounts to sweeten the deal. Here’s what you can expect:

- Multi-Policy Discounts: Bundling home and auto insurance for cost savings.

- Safe Driver Discounts: Reduced rates for maintaining a good driving record.

- Loyalty Discounts: Savings for customers who stick with their provider over time.

- Membership Discounts: Reductions for being a part of certain organizations or groups.

These discounts not only help you save but also make the policies more appealing by adding value.

The Role of Customer Service in Decision Making

The importance of stellar customer service in the insurance world can’t be overstated. A friendly and efficient service team can often make the difference in high-stakes situations like filing a claim or seeking advice. Always consider how an insurance provider’s customer interaction aligns with your expectations.

“The richest coverage isn’t worth much without a team that stands ready to support you when needed most.”

Whether it’s through 24/7 helplines or personalized support, a provider’s commitment to service excellence is a crucial component of the decision-making process.

Methods to Lower Insurance Rates

Are you tired of paying exorbitant insurance premiums? Lowering your insurance rates doesn’t have to feel like magic; with some savvy strategies, you can keep more money in your pocket without sacrificing coverage.

Understanding the elements that impact your insurance costs is key. Whether it’s your driving history or the power of bundling policies, there are actionable methods you can implement today to see significant savings.

Utilizing Safe Driving Records for Better Rates

Your driving record is more than just a history—it’s a resume that speaks volumes to insurance companies. A clean record not only paints you as a reliable driver but also directly decreases your risk profile. Less risk means lower premiums. If you maintain a record free from accidents and violations, insurers perceive you as a lower risk, translating into tangible savings.

Improving Credit Scores

The state of North Carolina often leverages credit scores to determine insurance rates. The table below highlights the potential impact:

| Credit Score Range | Insurance Rates Adjustment |

|---|---|

| 800-850 | Lowest possible rates |

| 740-799 | Below-average rates |

| 670-739 | Average rates |

| 580-669 | Above-average rates |

| 300-579 | Highest rates |

Optimizing your credit score can be a powerful tool in reducing your insurance costs. Insurers associate higher credit scores with lower risk. Aim to improve your score by paying bills on time, reducing overall debt, and keeping credit card balances low.

Bundling Policies for Maximum Savings

Mix and match your insurance plans! Bundling different insurance policies, such as home and auto, with the same provider can unlock discounts. For example, bundling homeowners and car insurance might save you anywhere from 5% to 25% on premiums. Not only does it streamline your coverage management, but it also offers a single deductible, making life a bit simpler and more cash-friendly.

“Bundling is the superpower of strategic savings, often overlooked but massively impactful.”

So, if you’re looking to cut costs without cutting corners, bundling could be your golden ticket.

Legal and Regulatory Framework

Navigating the intricate labyrinth of insurance regulations in North Carolina can be daunting, but understanding the legal framework is crucial for securing the best rates and complying with state laws. Here, we unravel the essential components of the state’s insurance landscape.

North Carolina mandates specific insurance requirements that all drivers must adhere to, ensuring both personal protection and public safety. These requirements lay out the minimum thresholds, and failing to comply can lead to serious repercussions.

Minimum Insurance Requirements in NC

In North Carolina, the law mandates that drivers carry a minimum amount of liability insurance. This ensures adequate coverage for potential damages or injuries caused in an accident. The requirements include:

- Bodily Injury Liability: $30,000 per person and $60,000 per accident.

- Property Damage Liability: $25,000 per accident.

- Uninsured Motorist Coverage: Equal to the policy’s bodily injury liability.

These thresholds are designed not just for compliance, but to safeguard financial stability and responsibility.

The Role of the North Carolina Department of Insurance

The North Carolina Department of Insurance plays a pivotal role in regulating and overseeing insurance providers and their rate offerings. The department’s mission transcends mere enforcement; it strives to ensure fairness and transparency in the marketplace.

The department’s commitment to consumer protection is reflected in its strict oversight of insurance rates and practices.

By scrutinizing proposed rate changes and ensuring alignment with regulatory standards, the department fosters a competitive and equitable environment for both providers and consumers alike.

Consequences of Non-compliance

Bearing the financial burden of violations is a stern reminder of the consequences of non-compliance with insurance regulations in North Carolina.

- Fines: Penalties for failing to meet the minimum insurance requirements.

- License Suspension: Driving privileges could be revoked, complicating daily life.

- Insurance Penalty Fees: Additional costs that exacerbate financial strain.

- Legal Ramifications: Potential lawsuits and legal fees from uninsured accidents.

These repercussions underscore the importance of maintaining valid insurance coverage at all times.

Recent Legislative Changes Affecting Insurance Rates

Legislation is a dynamic force, reshaping the insurance landscape to better reflect the needs of consumers and market conditions. Recent changes include:

- Introduction of telematics-based insurance options.

- Enhanced consumer data protection measures.

- Adjustments in minimum coverage limits to reflect economic changes.

- Encouragement of green insurance practices.

Staying informed about these legislative amendments helps in anticipating changes in insurance rates.

Customizing Insurance Policies

In the dynamic world of insurance, North Carolina residents have the unique opportunity to tailor policies that cater specifically to their life’s rhythms and needs. Customization empowers policyholders to craft coverage that is as individualized as their circumstances.

Customizing your insurance policy involves analyzing your current lifestyle and anticipating future needs, allowing you to select complementary coverage options that truly matter. The flexibility of these policies means you’re never overpaying for pointless perks or leaving gaps in essential coverage.

Exploring Premium Customization Options

Customization in insurance policies can transcend the standard offerings, allowing you to specify coverages that align with personal needs. The key benefits of customized plans include:

- Flexibility: Add or remove elements based on life changes.

- Financial Efficiency: Only pay for what you need.

- Enhanced Protection: Ensure coverage areas that standard policies might neglect.

The Benefits and Drawbacks of Tailored Insurance Plans

While customizable insurance plans offer many advantages, they also come with considerations:

- Benefits: Tailored to personal risks, lifestyle, and financial capability, a custom plan ensures optimal protection.

- Drawbacks: Over-customization can lead to confusion about coverage limits, and specialized policies might increase premium costs.

Guiding Choices: What to Add Beyond Basic Coverage

When amplifying your policy beyond the basics, choose additions that truly enrich your protection strategy. Consider these extras:

- Roadside Assistance: Ideal for frequent travelers or long commutes.

- Rental Reimbursement: A savior when your vehicle is in repair.

- Identity Theft Protection: Crucial in the digital age where cyber threats loom large.

| Customization Option | Benefit | Best Scenario |

|---|---|---|

| Roadside Assistance | Immediate help on breakdowns | Daily commuters and road trippers |

| Rental Reimbursement | Avoids travel disruptions when vehicle is unserviceable | Those reliant on personal vehicle for daily tasks |

| Identity Theft Protection | Safeguards personal information | Individuals active online and in retail transactions |

“Tailor your insurance just like you would a bespoke suit – fit for your unique lifestyle and perfectly adjusted to your personal risks.”

Exploring the Claims Process

Venturing into the realm of insurance claims can often feel like navigating a labyrinth, especially when you’re in a time of need. Whether it’s an auto mishap or a home incident, knowing the stepping stones of the claims process in North Carolina can transform confusion into clarity.

Understanding these steps not only ensures a smoother experience but can also safeguard you against unwanted hikes in your future insurance premiums. Let’s delve into the essential steps one must follow to file an insurance claim successfully in NC, and identify how each step may impact your rates.

Steps to Claim Filing in NC

Filing an insurance claim is more than just ticking boxes; it’s about ensuring each step is followed meticulously to maximize your benefits while minimizing any adverse rate effects.

| Steps | Description | Impact on Rates |

|---|---|---|

| Notification | Contact your insurance provider immediately after an incident to inform them about the situation. | Minimal immediate impact, but delays can increase scrutiny and potential rate hikes. |

| Documentation | Collect all necessary documentation—photos, police reports, witness statements to support your claim. | Comprehensive evidence helps prevent disputes—failed documentation can lead to rate increases. |

| Assessment | Your insurer will assess the claim to determine coverage and liability. | Reliable claims processing often has less impact on future rates; frequent or large claims might escalate costs. |

| Resolution | Receive settlement or claim denial, coupled with rationale if the latter occurs. | Resolved claims without issues keep rates steady, whereas contentious claims can trigger surcharges. |

Avoiding Common Pitfalls

In the complex world of claims, even the smallest missteps can become larger hurdles. Avoiding these can significantly enhance your experience.

- Procrastination: Delaying claim submission often leads to suspicion and scrutiny.

- Incomplete Documentation: Missing details can lead to claim denials or partial payouts—keep a meticulous record.

- Underestimating Damages: Assessments should be as accurate as possible to avoid insufficient compensation.

Remember, a well-documented claim is half the battle won.

The Impact of Claims on Future Rates

Each claim acts as a piece of your insurance puzzle—it can either fit seamlessly or disrupt the entire picture.

While single, infrequent claims typically don’t cause drastic rate changes, multiple claims or severe incidents can alert insurers to increased risk. Here are some factors that influence how your claims affect future rates:

- Claim Frequency: A pattern of frequent claims prompts insurers to label you as a high-risk client.

- Claim Type: Some claims, like comprehensive auto claims due to natural disasters, may affect your rates less than at-fault collisions.

- Claim Amount: Large claims signify a higher financial risk; thus, they might trigger noticeable premium increments.

By staying vigilant in understanding and managing these factors, you can negotiate the murky waters of insurance claims in North Carolina with confidence and poise.

Last Word

Congratulations, you’ve now unraveled the maze of insurance in North Carolina! Armed with this newfound wisdom, you’re set to glide effortlessly through the world of policies and premiums. Remember, the power to secure the best rates lies in your hands. Make informed choices, ask the right questions, and don’t hesitate to leverage discounts and customization options. Here’s to a future of smart savings and ultimate coverage!

FAQ Section

What types of insurance are available in North Carolina?

In North Carolina, you can find various insurance types including auto, health, homeowner’s, renter’s, and life insurance, each catering to different needs and legal requirements.

How can I lower my insurance premiums in NC?

Effective strategies include maintaining a good credit score, bundling different types of insurance, and ensuring a clean driving record.

Do driving records affect insurance rates in NC?

Yes, your driving record is a significant factor in determining your insurance premiums. A clean record typically results in lower rates.

What are the benefits of customizing my insurance policy?

Customizing your insurance policy allows you to tailor coverage according to your specific needs, potentially saving you money while ensuring adequate protection.

How important is customer service in choosing an insurance provider?

Customer service is crucial as it can significantly affect your experience, especially during claims processing. Providers with excellent customer support tend to make the process smoother and more satisfactory.